Small-town users fuel IPO-bound Moneyview's growth

Moneyview is experiencing a surge in credit demand from smaller cities. The firm's revenue from operations has more than tripled from ₹648 crore in FY23 to ₹2,339 crore in FY25. Loan disbursals compounded annually at 46% between FY23 and FY25, reaching ₹17,621 crore.

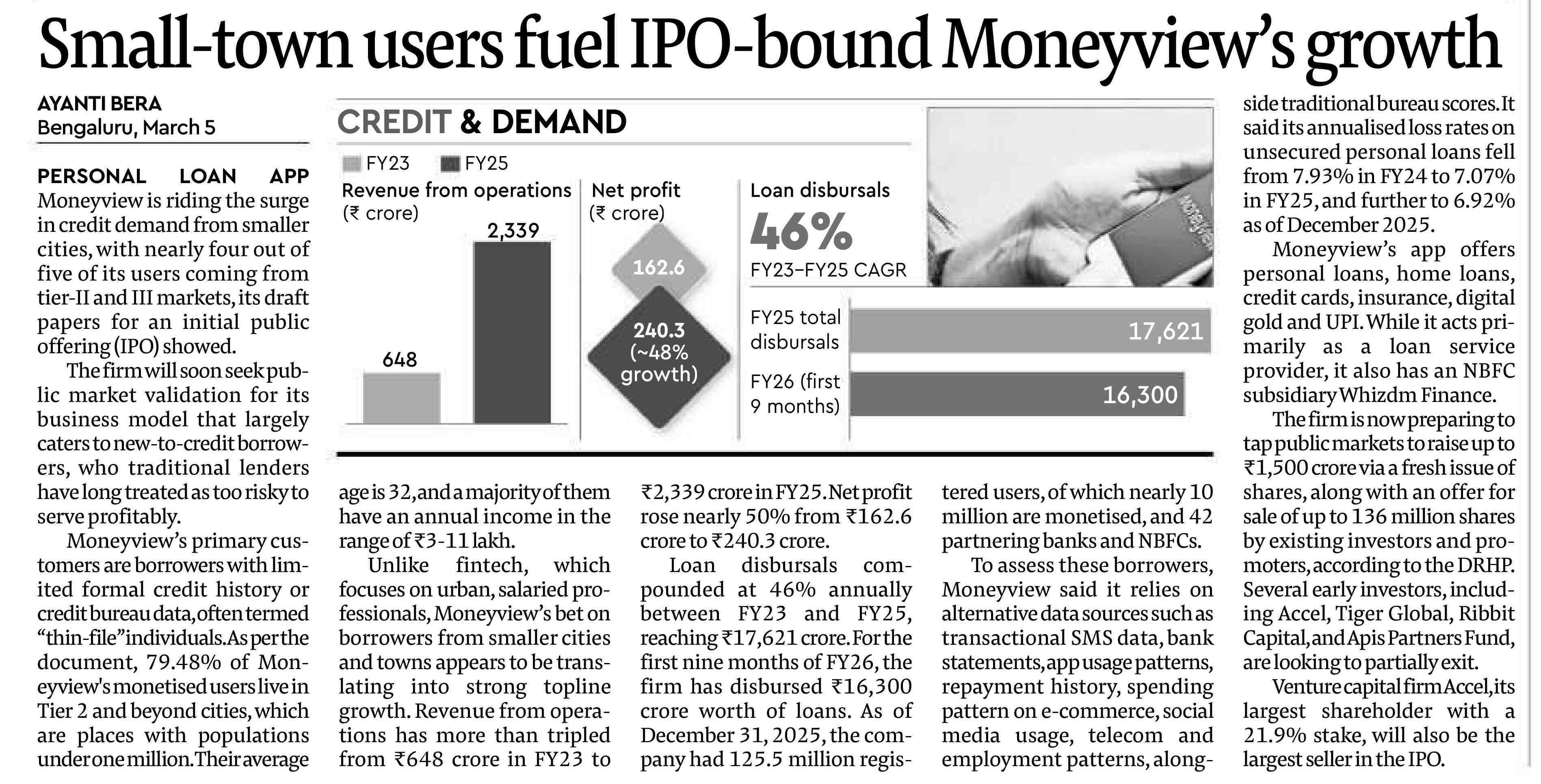

Small-town users fuel IPO-bound Moneyview's growth AYANTI BERA Bengaluru, March 5 PERSONAL LOAN APP Moneyview is riding the surge in credit demand from smaller cities, with nearly four out of five of its users coming from tier-II and III markets, its draft papers for an initial public offering (IPO) showed. The firm will soon seek public market validation for its business model that largely caters to new-to-credit borrowers, who traditional lenders have long treated as too risky to serve profitably. Moneyview's primary customers are borrowers with limited formal credit history or credit bureau data, often termed "thin-file" individuals. As per the document, 79.48% of Moneyview's monetised users live in Tier 2 and beyond cities, which are places with populations under one million. Their average age is 32, and a majority of them have an annual income in the range of 3-11 lakh. Unlike fintech, which focuses on urban, salaried professionals, Moneyview's bet on borrowers from smaller cities and towns appears to be translating into strong topline growth. Revenue from operations has more than tripled from ₹648 crore in FY23 to ₹2,339 crore in FY25. Net profit rose nearly 50% from ₹162.6 crore to ₹240.3 crore. Loan disbursals compounded at 46% annually between FY23 and FY25, reaching 17,621 crore. For the first nine months of FY26, the firm has disbursed ₹16,300 crore worth of loans. As of December 31, 2025, the company had 125.5 million registered users, of which nearly 10 million are monetised, and 42 partnering banks and NBFCs. To assess these borrowers, Moneyview said it relies on alternative data sources such as transactional SMS data, bank statements, app usage patterns, repayment history, spending pattern on e-commerce, social media usage, telecom and employment patterns, alongside traditional bureau scores. It said its annualised loss rates on unsecured personal loans fell from 7.93% in FY24 to 7.07% in FY25, and further to 6.92% as of December 2025. Moneyview's app offers personal loans, home loans, credit cards, insurance, digital gold and UPI. While it acts primarily as a loan service provider, it also has an NBFC subsidiary Whizdm Finance. The firm is now preparing to tap public markets to raise up to *1,500 crore via a fresh issue of shares, along with an offer for sale of up to 136 million shares by existing investors and promoters, according to the DRHP. Several early investors, including Accel, Tiger Global, Ribbit Capital, and Apis Partners Fund, are looking to partially exit. Venture capital firm Accel, its largest shareholder with a 21.9% stake, will also be the largest seller in the IPO. CREDIT & DEMAND FY23 FY25 Revenue from operations Net profit (₹ crore) (₹ crore) 648 2,339 162.6 240.3 (~48% growth) Loan disbursals 46% FY23-FY25 CAGR FY25 total disbursals 17,621 FY26 (first 9 months) 16,300